Written by: Benjamin Bimson CIMA®, CMT® / CIO, Trek Financial

Written by: Benjamin Bimson CIMA®, CMT® / CIO, Trek Financial

Bond yield curve inversion has a center stage on Wall Street these days. It demands attention and headlines, but why?

What exactly is an inverted yield curve? An inversion is technically when a shorter duration bond has a higher interest rate yield than a longer-term bond. It may sound odd that a bond investor could receive a greater compensation for holding a shorter maturity than a long, but it does happen, especially late in a business cycle.

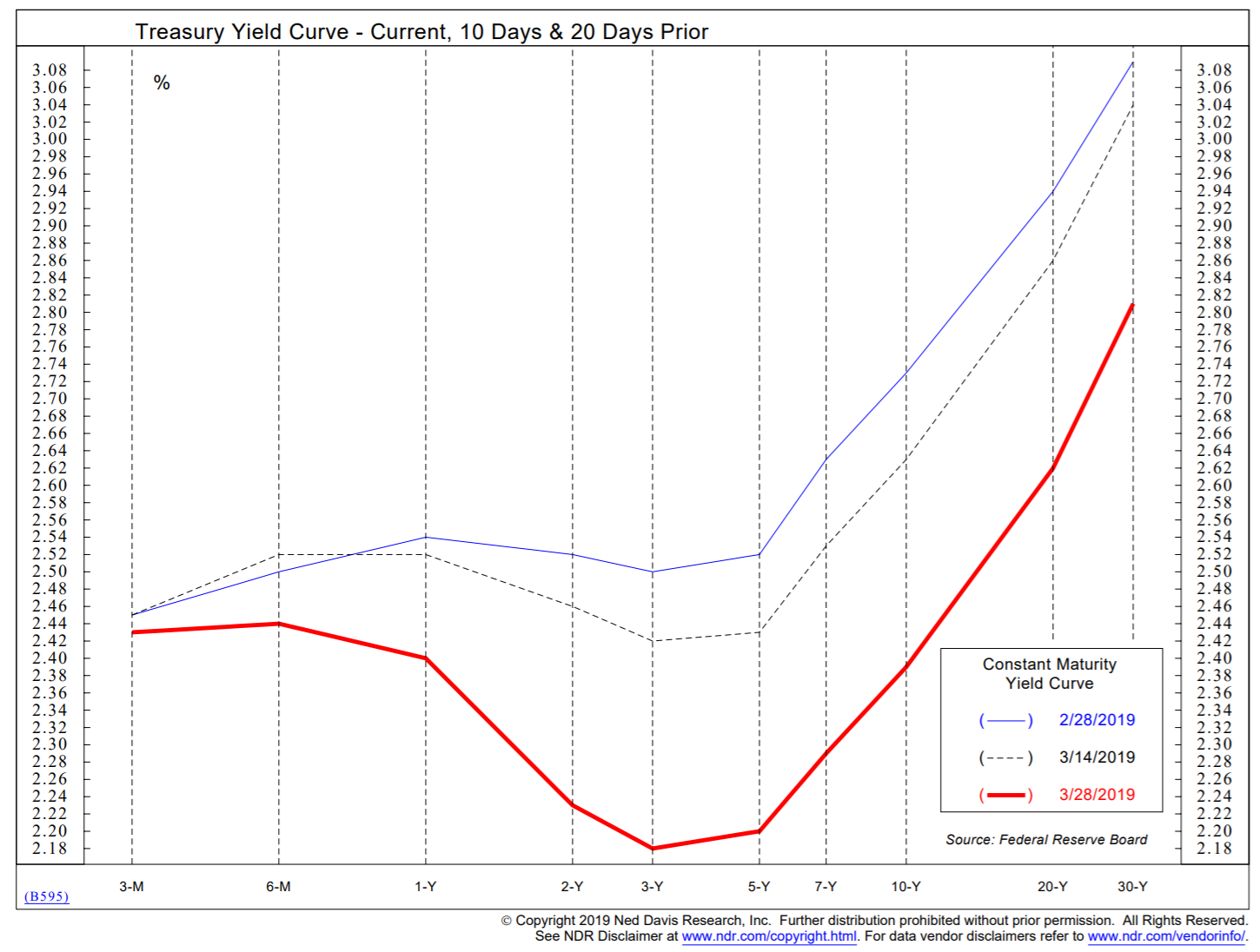

Though we do in fact have an inverted yield curve, the current curve is inconclusive. The most current and reliable measurement of yield curve inversion is the difference between the 6 month and 10-year Treasury bond. Currently the inverted yield curve is mostly in the 3-5-year range.

Progression of the yield conversion thus far. Copyright 2019 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

This is not to say that the inversion does not tell us anything, but we always must guard against using only one data-point to draw conclusions. It is much more likely that this inversion is just confirming what the market expects the next Fed moves are going to be.

There are a few things we can infer from current political banter as well as the latest Fed policy meeting notes. The Fed officially expected to end the bond runoff it began in October 2017, which means that there is likely a supply/demand imbalance on the shorter-term maturities. There is also a high likelihood that long-term inflation stays low for quite some time. Forward interest rate swaps are not perfect, but currently they imply a forward inflation expectation that are within the Federal Reserve’s neural range of 2-2.5%.

Interest rate expectations using forward swaps. Copyright 2019 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.

See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/.

Additionally, there is growing political pressure for Modern Monetary Theory (MMT). This is the idea that governments, like the U.S., can not default on debt since they also have the power to print money. This theory is introduced by political ideas like Medicare for all, the Green New Deal and Standard Basic Income (amongst other ideas). While the current political landscape does not yet support these ideas becoming law, it is rising in popularity among some voters. This would directly challenge and change our monetary system and the usefulness of certain data-points, like yield curves, could dramatically change.

The last point that we cannot lose sight of is that not every inversion on the yield curve has led to a recession. When it does, the average months prior to a recession is 15 months. When the 10-year minus 2-year Treasury bond inverts, the average months prior to a recession is 21 months in the past 5 recessions.1 Therefore, we continue to look at the weight of the evidence before we draw too many conclusions.

A recession seems likely, but we don’t yet have enough data to say it is imminent. It could be just as likely to be projecting a slowing economy and a change in Fed policy direction. This will certainly remain a focus from our perspective as well as much of the investment world. However, until the evidence proves otherwise, the market expansion is not yet over. We are likely late in the expansion, after all we are approaching a historical longest-bull market title. How long it can go will depend a lot on where the Fed moves next, geopolitical risks and tensions around the 2020 presidential election cycle.

View More Articles

Sources:

1-https://lplresearch.com/2019/03/28/11-things-you-need-to-know-about-the-yield-curve/

Investment advisory services are offered through Trek Financial, LLC., an SEC Registered Investment Adviser. Information presented is for educational purposes only. It should not be considered specific investment advice, does not take into consideration your specific situation, and does not intend to make an offer or solicitation for the sale or purchase of any securities or investment strategies. Investments involve risk and are not guaranteed, and past performance is no guarantee of future results. For specific tax advice on any strategy, consult with a qualified tax professional before implementing any strategy discussed herein. Trek FG 19-54